Skip to main content

Skip to main content

What Is My Whistleblower Case Worth?

Table of Contents

By Jason T. Brown, Managing Partner, Brown, LLC

General information only. This article is not legal advice. Whistleblower case value depends on statute, facts, proof, timing, collectability, agency interest, and risk.

Most whistleblower articles give the reward percentage and stop there. That is not valuation. That is marketing math.

A False Claims Act relator may receive 15% to 30% of the government recovery. SEC, CFTC, and FinCEN-style programs generally use 10% to 30% of collected monetary sanctions. IRS awards are generally tied to proceeds collected because of the whistleblower’s information. Those percentages matter. But they do not answer the real question.

The real question is: what is the risk-adjusted value of the case?

A theoretically huge case can have very little practical value if the proof is weak, the government already knows, another relator filed first, the defendant cannot pay, the damages model is speculative, or the whistleblower mishandled evidence. A smaller case with clean documents, a solvent defendant, a clear payment link, and strong government interest can be worth more.

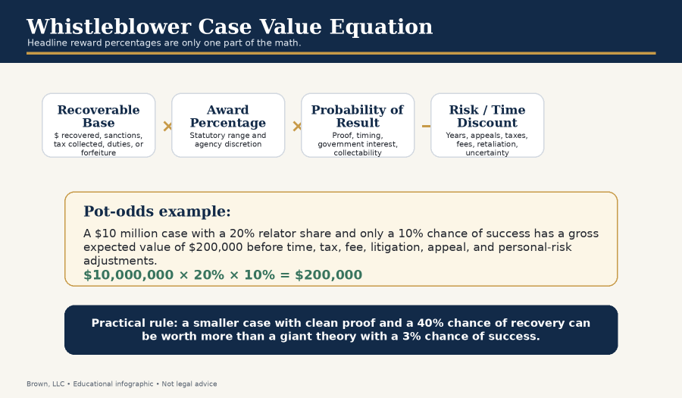

Short answer: a whistleblower case is worth recovery times share times odds, minus risk

The simplest useful model is this:

Estimated case value = potential recovery × likely award percentage × probability of success − time/risk/tax/fee/personal-cost adjustments.

For example, a $10 million recovery theory with a 20% relator share sounds like a $2 million case. But if the case has only a 10% chance of producing a recovery, the gross expected value is $200,000 before taxes, fees, delay, appeals, retaliation, stress, and collection risk.

That is what I mean by pot odds. You do not just ask “how big is the pot?” You ask how much you must risk, how often the hand wins, and whether the payout justifies the path.

The four numbers that matter

A serious valuation starts with four numbers.

1. The recoverable base

This is not always the same as the fraud amount. In an FCA case, the base may involve single damages, treble damages, statutory penalties, settlement discount, and the defendant’s ability to pay. In an SEC or CFTC case, the base is monetary sanctions collected in a covered action or related action. In an IRS case, the base is proceeds actually collected. In customs or tariff cases, the base may be unpaid duties, penalties, and other government losses. In FinCEN or AML matters, the base is expected to be monetary sanctions collected in qualifying enforcement actions as the program matures.

2. The award percentage

For FCA cases, the statutory range is generally 15% to 25% where the government proceeds with the case and 25% to 30% where the government does not proceed and the relator successfully conducts the action. The FCA also allows reductions for certain public-disclosure cases and for relators who planned and initiated the violation. A related criminal conviction can eliminate the share entirely. [Sources: 31 U.S.C. § 3730; DOJ FCA statistics.]

For SEC cases, the statutory range is 10% to 30% of collected monetary sanctions, but the SEC applies factors such as significance of information, assistance, law-enforcement interest, delay, culpability, and interference with internal compliance. [Sources: 15 U.S.C. § 78u-6; SEC FY2025 annual report.]

For CFTC cases, the award range is also 10% to 30% of collected sanctions, and the CFTC expressly considers significance, assistance, law-enforcement interest, internal reporting, culpability, delay, and interference. [Sources: 17 CFR §§ 165.8, 165.9.]

For IRS cases, the practical issue is collected proceeds. The IRS FY2024 report states that the IRS paid $123.5 million in awards attributable to $474.7 million in collected proceeds, and that awards paid were 26.0% of proceeds collected that year. [Source: IRS FY2024 annual report.]

3. The probability of a result

This is the part most online calculators ignore. Most tips, claims, and complaints do not become paid awards. The public data does not give a perfect cohort win rate because cases filed in one year may resolve years later. Still, public program data gives useful reality checks.

4. The risk discount

A whistleblower case can take years. It can trigger retaliation. It can involve sealed litigation, agency silence, appeals, award disputes, tax issues, privilege questions, document-handling risk, and emotional cost. If your own conduct could be questioned, the analysis becomes even more complex.

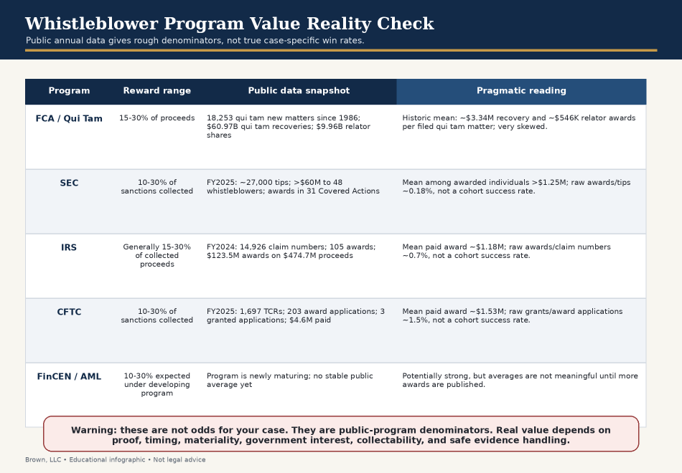

Public data reality check: average awards and raw odds are useful, but dangerous if misread

The table below uses public annual statistics. It does not predict any individual case. It also mixes different denominators because each program reports differently. Treat it as a reality check, not a promise.

| Program | Public value data | Raw result data | Pragmatic reading |

| False Claims Act / Qui tam | From 1986 through FY2025, the DOJ reports $60.97B in qui tam settlements and judgments and $9.96B in relator share awards. Across 18,253 qui tam new matters, that is about $3.34M in recovery and $546K in relator share per filed matter on a crude historical average. | FY2025 had 1,297 new qui tam suits and $5.34B in recoveries from those and earlier-filed qui tam suits. This is not a same-year win rate because old cases resolve in later years. | The mean is inflated by huge cases. Many filed cases produce zero. Strong cases need proof, materiality, damages, timing, government interest, and collectability. |

| SEC | In FY2025, the SEC awarded more than $60M to 48 individual whistleblowers in 31 Covered Actions. That is more than $1.25M per awarded individual using the $60M floor. | The SEC received about 27,000 tips in FY2025. A crude awarded-individuals/tips comparison is about 0.18%, but this is not a cohort win rate and a large share of tips comes from a small number of repeat filers. | The SEC can produce major awards, but most tips do not become awards. Originality, timing, and usefulness are central. |

| IRS | In FY2024, the IRS paid $123.5M across 105 awards, about $1.18M per paid award, on $474.7M in collected proceeds. | The IRS built 14,926 claim numbers in FY2024. A crude awards/claim-numbers comparison is about 0.7%, but not a cohort win rate. | IRS cases live or die on tax underpayment, collectability, proof, and patience. The case may be large on paper but worthless if the IRS cannot collect. |

| CFTC | In FY2025, CFTC issued two award orders granting three applications totaling $4.6M, about $1.53M per granted application. | CFTC received 1,697 TCRs and 203 award applications in FY2025. Three grants equals about 1.5% of applications or 0.18% of TCRs, not a cohort win rate. | CFTC cases can be strong, but the denominator is harsh. Timely, specific, market-useful information matters. |

| FinCEN / AML | The program is still maturing. The proposed rule and statute contemplate awards tied to monetary sanctions for covered AML/sanctions violations. | No stable public average exists yet. | Do not sell certainty here. AML/sanctions cases may be high-value, but the public award history is not mature enough for reliable averages. |

Why average whistleblower values mislead people

Average whistleblower values are distorted by outliers. A few giant healthcare, pharma, defense, tax, securities, or customs matters can make the average look far better than the experience of most claimants. Averages also ignore dismissed cases, declined cases, tips that never become investigations, award denials, settlements that allocate money away from the whistleblower’s claim, and cases where the defendant cannot pay.

For that reason, Brown, LLC looks less at “average settlement” and more at expected value: the size of the potential recovery, multiplied by the realistic chance of getting to that recovery, adjusted for risk and time.

The pot-odds approach to whistleblower valuation

Suppose two potential FCA cases come in.

Case A has a $100 million theory. But the proof is circumstantial, the government already audited the issue, materiality is disputed, and the defendant has strong defenses. If the chance of a real recovery is 5%, a 20% relator share produces a gross expected value of $1 million.

Case B has a $25 million theory. But the whistleblower has internal emails, clear invoices, a strong payment link, a solvent defendant, and a clean first-to-file position. If the chance of a real recovery is 25%, a 20% share produces a gross expected value of $1.25 million.

Case B may be the better case even though Case A sounds larger. That is pot odds.

False Claims Act case value: the highest ceiling, but still hard

FCA cases are often the most valuable whistleblower cases because damages can include treble damages and civil penalties, and because relators may receive 15% to 30% of proceeds depending on government intervention and other factors.

But the headline number is not the settlement number. The government may settle for less than theoretical treble damages. Penalties may be negotiated. Some money may be excluded from relator share calculations. A defendant may be unable to pay. the DOJ may decline to intervene. Another relator may have filed first. A court may find materiality lacking. A defendant may win on scienter, causation, public disclosure, or Rule 9(b).

The strongest FCA value drivers are: substantial government loss, specific false claims or false statements, strong proof of knowledge, clear materiality, recent or ongoing conduct, a solvent defendant, and a whistleblower who can help the DOJ understand the case.

Healthcare FCA value: huge ceiling, more scrutiny

Healthcare FCA cases produce some of the largest recoveries, but they are also heavily defended. The best cases usually involve a clear bridge from misconduct to federal payment: diagnosis codes, claims data, kickbacks, medical necessity, cost reports, Medicare Advantage risk adjustment, pharmacy claims, or billing certifications.

A healthcare case with a billion-dollar theory but weak clinical proof may be less valuable than a narrower case with clean patient-level examples, internal emails, and claims data.

Cyber-FCA value: fast-growing, but technical proof is everything

Cybersecurity whistleblower cases can be valuable where a contractor’s government-facing cyber representation does not match technical reality. The value usually turns on the gap between what the company told the government and what engineers, ISSOs, security leads, SSPs, POA&Ms, SPRS scores, FedRAMP files, CMMC records, or incident reports show internally.

A vague claim that “security is bad” is not enough. A strong cyber-FCA case explains the contract requirement, the certification, the actual control gap, who knew, why it mattered to payment or eligibility, and where the proof is.

SEC case value: large awards, brutal filtering

SEC awards can be very large. But the denominator is severe. The SEC received about 27,000 whistleblower tips in FY2025 and awarded more than $60 million to 48 individual whistleblowers in 31 Covered Actions. That is a reminder that most tips do not become awards, and many award claims are denied for lack of voluntariness, lack of original information, or failure to lead to the successful covered action.

SEC case value increases when the information is original, early, specific, useful, tied to investor harm or market integrity, supported by documents, and presented before the SEC or another listed authority asks for it.

IRS case value: the most misunderstood value calculation

IRS whistleblower cases are not valued on alleged tax loss alone. They are valued on proceeds collected and attributable to the whistleblower’s information. That makes collectability central.

A $100 million tax-loss theory may be practically weak if the taxpayer is insolvent, offshore, dissolved, protected by legal defenses, or already under IRS scrutiny. A $20 million tax case with clean records, a solvent taxpayer, strong assets, and a clear tax theory may be better.

For Brown, LLC to invest serious time in an IRS whistleblower case, the matter generally needs to be large, collectable, and provable. A practical screen is at least $10 million in likely federal tax underpayments or collectable proceeds, realistic collectability, and solid proof. That is a firm-intake screen, not the IRS statutory threshold.

CFTC case value: useful for commodities and crypto-market insiders, but not a volume play

CFTC whistleblower cases can involve commodities, derivatives, swaps, manipulation, spoofing, crypto commodities, market abuse, and related misconduct. The award range is 10% to 30% of collected sanctions, but the CFTC data shows a hard funnel. In FY2025, CFTC received 1,697 TCRs and 203 award applications, but granted three applications totaling $4.6 million.

The best CFTC matters usually have specific trading records, market-impact evidence, communications, timing, and an insider who can help the agency understand complex transactions.

FinCEN, AML, and sanctions value: potentially big, but new enough to avoid hype

FinCEN’s whistleblower program is becoming important for BSA, sanctions, money laundering, IEEPA, TWEA, and Kingpin Act violations. But it is still too new for a stable average award value. The best way to frame AML value is not “average settlement.” It is whether the tip is timely, actionable, tied to covered violations, and connected to collectible sanctions.

High-value AML and sanctions cases may involve sanctions-screening overrides, suspicious-activity monitoring, correspondent banking, crypto flows, shell-company beneficial ownership, high-risk jurisdictions, or internal pressure to ignore red flags.

Retaliation value is a different case altogether

Do not mix reward-case math with retaliation-case math. Retaliation claims are usually valued around wage loss, benefits, emotional distress, reinstatement or front pay, statutory multipliers where available, fees, and leverage. A retaliation case can be important and valuable. But it usually does not have the same upside as a successful FCA, SEC, IRS, CFTC, AML, or customs award case.

Retaliation value is covered in a separate companion article on what a whistleblower retaliation case is worth, because the proof problems, headwinds, settlement posture, and demand-letter strategy are different.

What increases whistleblower case value

- A clear false statement or false claim.

- A direct payment, sanctions, tax, duties, investor, or forfeiture link.

- Internal documents or witnesses showing knowledge.

- Strong materiality.

- Substantial recoverable money.

- A solvent defendant.

- Original information not already known to the government.

- First-to-file or early-voluntary status.

- Clean evidence handling.

- Whistleblower credibility and useful ongoing assistance.

What destroys value

- Speculation without proof path.

- Public information that adds nothing new.

- Government already knows the essential facts.

- Another relator filed first.

- Weak materiality.

- Small damages or uncollectable defendant.

- Documents obtained unlawfully or in a way that creates privilege or taint issues.

- Whistleblower delay, culpability, obstruction, or inconsistent story.

- No clear program fit.

- Demanding a payout before understanding risk.

Why online whistleblower calculators can mislead

A calculator can show theoretical exposure. It cannot tell you whether the DOJ will intervene, whether SEC staff will use your information, whether the IRS can collect, whether the CFTC will credit your assistance, whether penalties will be negotiated down, whether another whistleblower filed first, whether the defendant can pay, or whether your documents can be used safely.

Use calculators for education. Do not use them as case valuation.

Why Brown, LLC evaluates value differently

Brown, LLC evaluates whistleblower value like a litigation and enforcement problem, not a lottery ticket. The firm looks at proof, statute fit, damages, materiality, first-to-file risk, public-disclosure risk, agency usefulness, collectability, defendant solvency, retaliation exposure, evidence handling, and the realistic probability of a result.

That approach is less exciting than “you could get 30%.” It is also more honest. Most whistleblower cases are not worth filing. The ones that are worth filing need to be built carefully.

What to bring to a whistleblower case-value consultation

- A short timeline.

- The actor: company, taxpayer, provider, contractor, issuer, bank, importer, trader, broker, or executive.

- The false statement or false claim.

- The affected program: Medicare, Medicaid, DoD, SEC investors, IRS, CFTC, CBP, FinCEN, sanctions, or another path.

- The money path.

- The proof path: where records, systems, witnesses, emails, claims, ledgers, filings, or submissions are located.

- Any internal warnings, audits, or objections.

- Whether the government already knows.

- Whether someone else may have reported.

- Your role and any exposure.

Bottom line

A whistleblower case is not worth the biggest number in the complaint. It is worth the recoverable base multiplied by the likely share multiplied by the odds of a result, adjusted for time, risk, taxes, fees, collectability, and personal cost.

If you want a serious answer to “what is my whistleblower case worth,” start with the evidence, the statute, the money path, and the odds. Then talk to counsel before reporting internally, contacting the government, or moving documents.

FAQ

How much do whistleblowers usually get paid?

It depends on the program and whether there is a successful recovery. FCA relators generally receive 15% to 30% of proceeds. SEC and CFTC whistleblowers generally receive 10% to 30% of collected sanctions. IRS whistleblower awards are generally tied to collected proceeds. Many tips and filed cases produce no award.

What is the average whistleblower settlement?

There is no reliable universal average. Public FCA historical data suggests about $3.34 million in qui tam recovery per filed qui tam matter and about $546,000 in relator awards per filed matter when all historical totals are divided by all historical qui tam new matters. That is not a prediction; it is a rough, skewed aggregate. SEC, IRS, and CFTC report tips, claims, awards, and sanctions differently, so direct averages can mislead.

Is a $10 million whistleblower case worth filing?

Maybe. A $10 million case with a 20% share and a 10% chance of success has a gross expected value of $200,000 before risk adjustments. It may be worth pursuing if proof is strong and risk is manageable. It may not be worth pursuing if the odds are low, the defendant is uncollectable, or the government already knows.

Can a smaller whistleblower case be better than a larger one?

Yes. Clean proof, strong timing, materiality, collectability, and government interest can make a smaller case more valuable than a giant but speculative theory.

Is retaliation value included in the reward calculation?

No. Retaliation value is separate. FCA retaliation under 31 U.S.C. § 3730(h), SEC/Dodd-Frank retaliation, SOX, OSHA-administered statutes, and state-law retaliation claims have their own damages models. They usually turn on wage loss, causation, proof, and leverage.

Source and Accuracy Confirmation

This article is based directly on the government program reports, statutes, regulations, and public filings listed in the Sources section below, and its factual statements have been checked against those sources. The award percentages, statutory ranges, and program data reflect the cited DOJ, SEC, IRS, CFTC, and FinCEN materials as published. The dollar figures, odds, and expected-value examples are illustrative and do not predict the outcome of any individual case. Where a program is still developing, such as the FinCEN whistleblower program, the article limits its claims to what the available public sources support and notes that no stable average award exists yet.

Sources

DOJ FCA FY2025 press release: https://www.justice.gov/opa/pr/false-claims-act-settlements-and-judgments-exceed-68b-fiscal-year-2025

DOJ FCA FY2025 fraud statistics PDF: https://www.justice.gov/opa/media/1424121/dl

False Claims Act, 31 U.S.C. § 3730: https://www.law.cornell.edu/uscode/text/31/3730

SEC FY2025 Office of the Whistleblower annual report: https://www.sec.gov/files/fy25-annual-whistleblower-report.pdf

SEC whistleblower statute, 15 U.S.C. § 78u-6: https://www.law.cornell.edu/uscode/text/15/78u-6

IRS Whistleblower Office FY2024 annual report: https://www.irs.gov/pub/irs-pdf/p5241.pdf

IRS Whistleblower Office: https://www.irs.gov/compliance/whistleblower-office

CFTC FY2025 Whistleblower report: https://www.whistleblower.gov/sites/whistleblower/files/2026-02/FY%202025%20Whistleblower%20%26%20Customer%20Education%20Report.pdf

CFTC whistleblower award amount rule, 17 CFR § 165.8: https://www.law.cornell.edu/cfr/text/17/165.8

CFTC award criteria, 17 CFR § 165.9: https://www.law.cornell.edu/cfr/text/17/165.9

FinCEN proposed whistleblower rule: https://www.federalregister.gov/documents/2026/04/01/2026-06271/whistleblower-incentives-and-protections

FinCEN whistleblower program: https://www.fincen.gov/whistleblower-program

DOJ Corporate Whistleblower Awards Pilot Program: https://www.justice.gov/criminal/criminal-division-corporate-whistleblower-awards-pilot-program

OSHA whistleblower statistics FY2018-FY2023: https://www.whistleblowers.gov/factsheets_page/statistics/FY2023

EEOC FY2024 Annual Performance Report: https://www.eeoc.gov/2024-annual-performance-report

EEOC retaliation guidance: https://www.eeoc.gov/laws/guidance/enforcement-guidance-retaliation-and-related-issues

Reuters, UBS whistleblower settlement after 13 years: https://www.reuters.com/business/ubs-settle-lawsuit-with-whistleblower-court-filings-show-2026-03-12/