Skip to main content

Skip to main content

How to Report Customs Fraud in 2026: FCA Qui Tam, CBP e‑Allegations, EAPA, and Moiety Claims

Table of Contents

Most customs-fraud pages ask the wrong question. They ask: What is customs fraud? That matters, but it is not the first question serious whistleblowers, competitors, and import insiders should ask. The first question is: Where should I report it?

That choice can change almost everything:

- whether the matter is handled under seal

- whether there is a serious whistleblower reward path

- whether CBP gets an immediate tip through its online portal

- whether an antidumping or countervailing duty case belongs in EAPA

- whether the matter is too small for a major False Claims Act filing but still worth a customs informant claim

- whether the government treats it as a civil customs-duty case, an administrative trade case, or a criminal trade-fraud matter

That is also why this is the strongest contemporary customs-fraud topic for Brown’s site. Existing customs pages already cover what customs fraud is, tariff-evasion theories, and why customs fraud can violate the False Claims Act. This page owns the decision-stage question those pages do not: which reporting route should be used, and when?

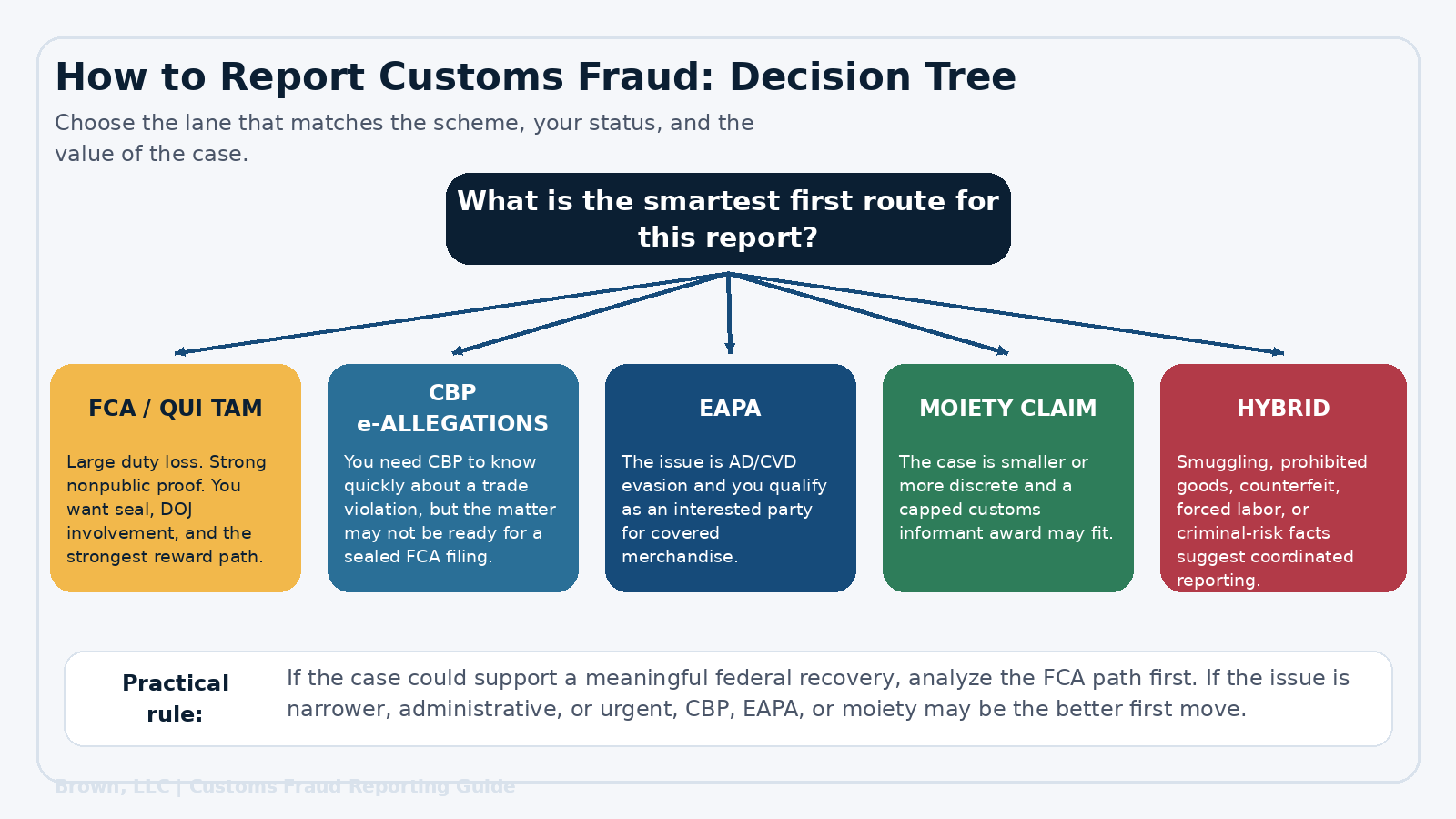

The Short Answer: Which Route Is Usually Best?

There is no single answer for every customs-fraud matter. But there is a practical answer. If the case is large, you have strong nonpublic facts, and reward, seal, and leverage matter, the False Claims Act is often the most powerful route.

If the issue is a broad trade violation or you need to alert CBP quickly, a CBP e‑Allegation may be the right first channel. If the case is specifically about antidumping or countervailing duty evasion, and the reporter qualifies as an interested party, EAPA may be the correct administrative route.

Speak with the Lawyers at Brown, LLC Today!

Over 100 million in judgments and settlements trials in state and federal courts. We fight for maximum damage and results.

If the case is smaller or more discrete and may support customs informant compensation rather than a major FCA recovery, a moiety claim may belong in the conversation. And if the conduct involves smuggling, prohibited goods, false country-of-origin schemes with criminal exposure, or other high-risk conduct, the smartest route may be a hybrid strategy involving DOJ, HSI, the FBI, CBP, and, in the right case, a sealed FCA filing.

The point is simple: do not treat these options as interchangeable. They are not.

Why This Question Matters More Now

Customs fraud is not a side issue anymore. Federal enforcement agencies have made that clear. DOJ and DHS launched a cross-agency Trade Fraud Task Force in August 2025. DOJ’s fiscal year 2025 False Claims Act announcement said the Department is focusing on the improper avoidance of tariffs and customs duties. Recent customs-duty settlements have also shown real money and real enforcement attention in this area.

That means insiders and competitors need to think more strategically. If the government is paying more attention, the cost of choosing the wrong reporting lane goes up. It also means companies are more likely to self-disclose, remediate, and try to get ahead of a whistleblower narrative. So timing matters.

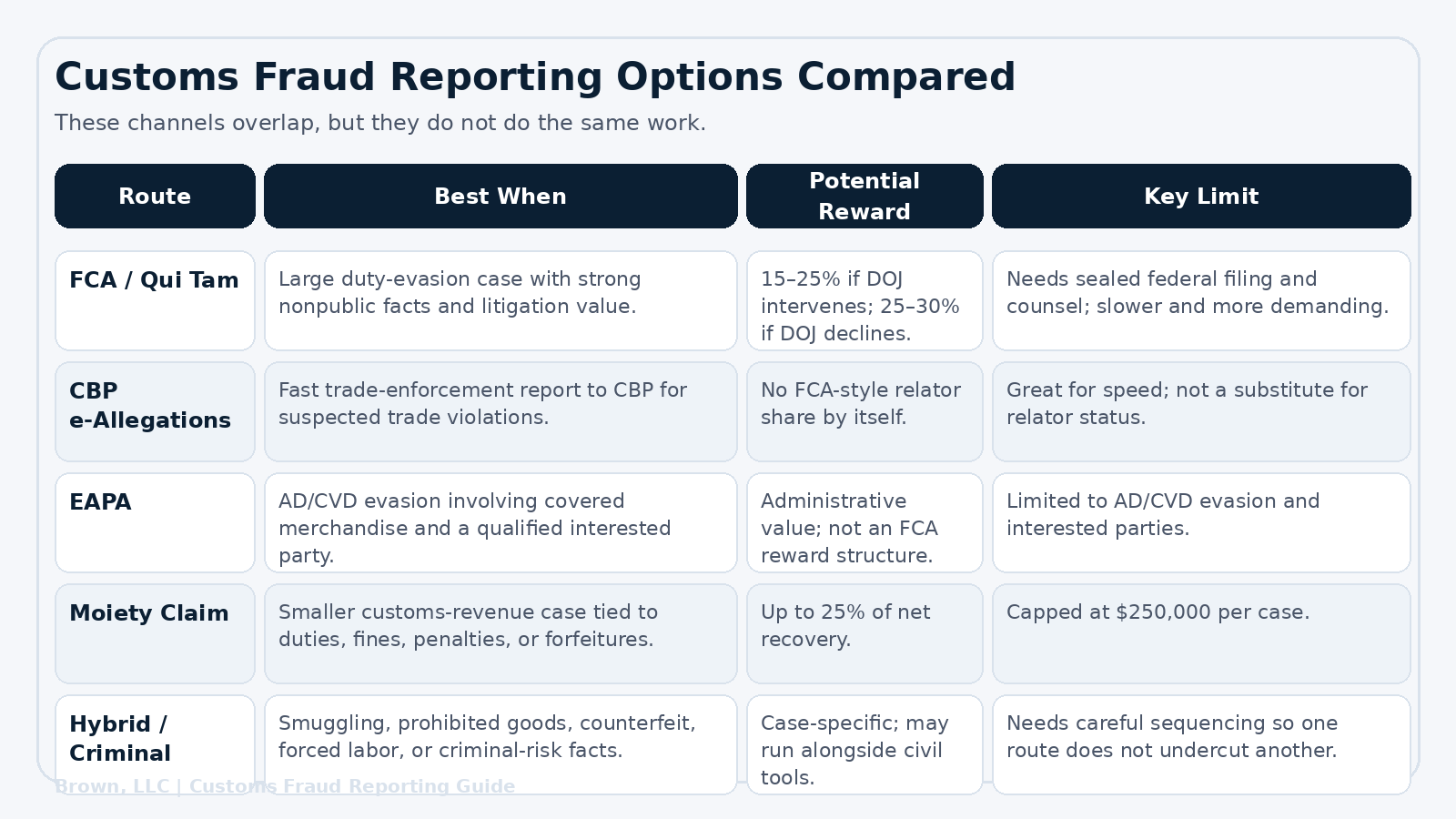

Route 1: File a Sealed False Claims Act Case

For many serious customs-duty cases, the False Claims Act is the strongest tool. The FCA is powerful because it does not just let the government sue. It also lets a private relator file a case under seal on behalf of the United States. The relator can receive a share of the government’s recovery. In a customs case, that usually means a reverse false claims theory: the importer knowingly used false statements or omissions to avoid paying money owed to the United States.

In plain terms, if a company knowingly dodged duties, tariffs, AD/CVD deposits, or other customs obligations through false paperwork or deliberate omissions, the FCA may fit.

Why the FCA Route Is Often the Best Route

A serious FCA customs case can offer:

- a sealed filing at the beginning of the case

- a relator share that can materially exceed administrative reward caps

- DOJ involvement

- leverage that a simple portal complaint does not create

- the ability to present the fraud as a coordinated litigation package, not just a raw tip

What Kinds of Customs Schemes Often Fit the FCA

Common customs-fraud patterns that may support an FCA theory include:

- false country-of-origin statements

- transshipment through third countries

- undervaluation and double-invoicing

- misclassification to reduce duties

- false statements about whether goods fall within an AD/CVD order

- sham “kits” or other packaging tactics designed to avoid scope coverage

- knowingly failing to correct customs declarations after learning they were false

Why Counsel Matters Here

An FCA case is not the same thing as sending a complaint to an agency. The complaint must be prepared and filed correctly. It must be filed under seal. The government must receive a written disclosure of the material evidence and information. And no one can prosecute an FCA case on behalf of the United States without following that statutory process.

That is why the first question in a large customs-duty case is often not “Should I send a tip?” It is: Should this be evaluated for a sealed qui tam filing before I do anything else?

Route 2: Report the Issue Through CBP E‑Allegations

A CBP e‑Allegation is a different tool. CBP’s Trade Violation Reporting system is designed for suspected trade violations. It is a real enforcement channel. It is also broader than a False Claims Act case. This route can make sense when:

- the reporter wants CBP to know about the conduct quickly

- the issue may not justify a sealed FCA filing

- the conduct involves trade violations that do not fit neatly into an FCA damages model

- the reporter is a competitor, customer, logistics participant, or other source who can point CBP in the right direction

- the concern includes issues like forced labor, counterfeit goods, de minimis abuse, false origin claims, or other trade violations that may call for fast agency attention

Why E‑Allegations Can Be Useful

The value of an e‑Allegation is speed and direct agency visibility. It is often the fastest official lane for getting suspected trade fraud in front of CBP. It is also useful when the reporter is not yet ready for a complex FCA presentation or when the case is more operational than litigation-driven.

The Major Limit of E‑Allegations

A CBP portal report is not the same thing as filing an FCA case. It does not create relator status under the False Claims Act. It does not itself secure an FCA relator share. It is a tip route, not a sealed litigation route. That distinction matters. If the case is large enough that a sealed FCA filing belongs in the conversation, the whistleblower should think very carefully before treating a portal report as the only move.

Route 3: Use EAPA if the Case Is AD/CVD Evasion and You Qualify

EAPA is not a general customs-fraud program. It is a targeted administrative regime for evasion of antidumping and countervailing duties. That is important. If the misconduct involves AD/CVD orders, EAPA may be the right lane. If it does not, EAPA may not be available at all.

EAPA is also not open to everyone. It is built around an interested party concept. That is why EAPA is often most useful for:

- domestic manufacturers or producers

- qualifying trade associations

- importers or foreign producers who meet the statutory and regulatory definitions

- other parties who fit the “interested party” category for covered merchandise

Why EAPA Can Be Powerful

EAPA gives qualified parties a focused path to force attention on AD/CVD evasion. The regulations expressly define evasion to include things like:

- transshipment

- misclassification

- undervaluation

when those acts reduce or eliminate applicable AD/CVD cash deposits or duties. The regulations also require that an allegation be filed through the appropriate CBP portal, limited to one importer per allegation, and supported by information reasonably available to the interested party. This is not a casual email process. It is a structured administrative route with its own rules.

When EAPA May Be Better Than a General CBP Tip

If the core issue is covered merchandise under AD/CVD orders, and the reporting party is a qualified interested party, EAPA can be a sharper tool than a general CBP complaint because it is built for that exact problem.

When EAPA Is Not Enough

EAPA is not a substitute for every customs whistleblower strategy. It does not cover all customs-duty fraud. It is not the right answer for every tariff or valuation issue. And if the case is large enough to support a serious FCA recovery, the whistleblower needs to think about whether the administrative route alone leaves too much value on the table.

Route 4: Consider a Moiety Claim for the Right Customs-Revenue Case

The customs moiety statute is one of the most overlooked parts of this field. Under 19 U.S.C. § 1619 and 19 C.F.R. § 161.16, an informant may be paid up to 25% of the net recovery to the government from duties withheld, fines, penalties, or forfeitures. But there is a major limit: the award cannot exceed $250,000 in any one case. That cap matters.

When a Moiety Claim May Make Sense

A moiety claim may make sense when:

- the matter is meaningful but not large enough to justify a full-scale FCA case

- the reporter wants a customs-specific informant route

- the case is tied to recoveries such as duties, penalties, or forfeitures

- the expected economics do not justify a large qui tam build-out

When It May Not Be Worth It

If the case could produce a large federal recovery, a capped $250,000 route may not be the best economic choice. That is why moiety claims are often best thought of as a customs informant lane, not as a replacement for a substantial FCA customs case.

One More Procedural Point

The current eCFR says a moiety claim is filed on DHS Form 4623 through HSI. CBP’s Trade Violation Reporting materials also indicate that a moiety claim should be tied to a related e‑Allegation or EAPA allegation. So again, this is its own lane. It is not the same thing as a sealed FCA case.

Route 5: Use a Hybrid Civil-Criminal Reporting Strategy When the Facts Justify It

Some customs cases are bigger than duty evasion alone. Some involve:

- smuggling

- prohibited goods

- false origin schemes tied to broader criminal conduct

- forced labor concerns

- counterfeit goods

- corporate self-disclosure or compliance failures that create overlapping civil and criminal exposure

DOJ’s own customs statements make clear that customs enforcement is increasingly coordinated across the Civil Division, Criminal Division, CBP, and HSI. That means the right answer is sometimes not one reporting channel. Sometimes the right answer is a planned sequence.

Examples:

- a sealed FCA case plus a tailored government presentation

- an EAPA filing plus related agency outreach

- a CBP tip plus criminal referral issues

- an FCA evaluation first, followed by decisions about whether and when other agencies should be engaged

This is where sophisticated counsel matters most. A whistleblower does not want to accidentally undercut a high-value FCA matter by using the wrong first channel. But the whistleblower also does not want to ignore an administrative or criminal route that would strengthen the government response.

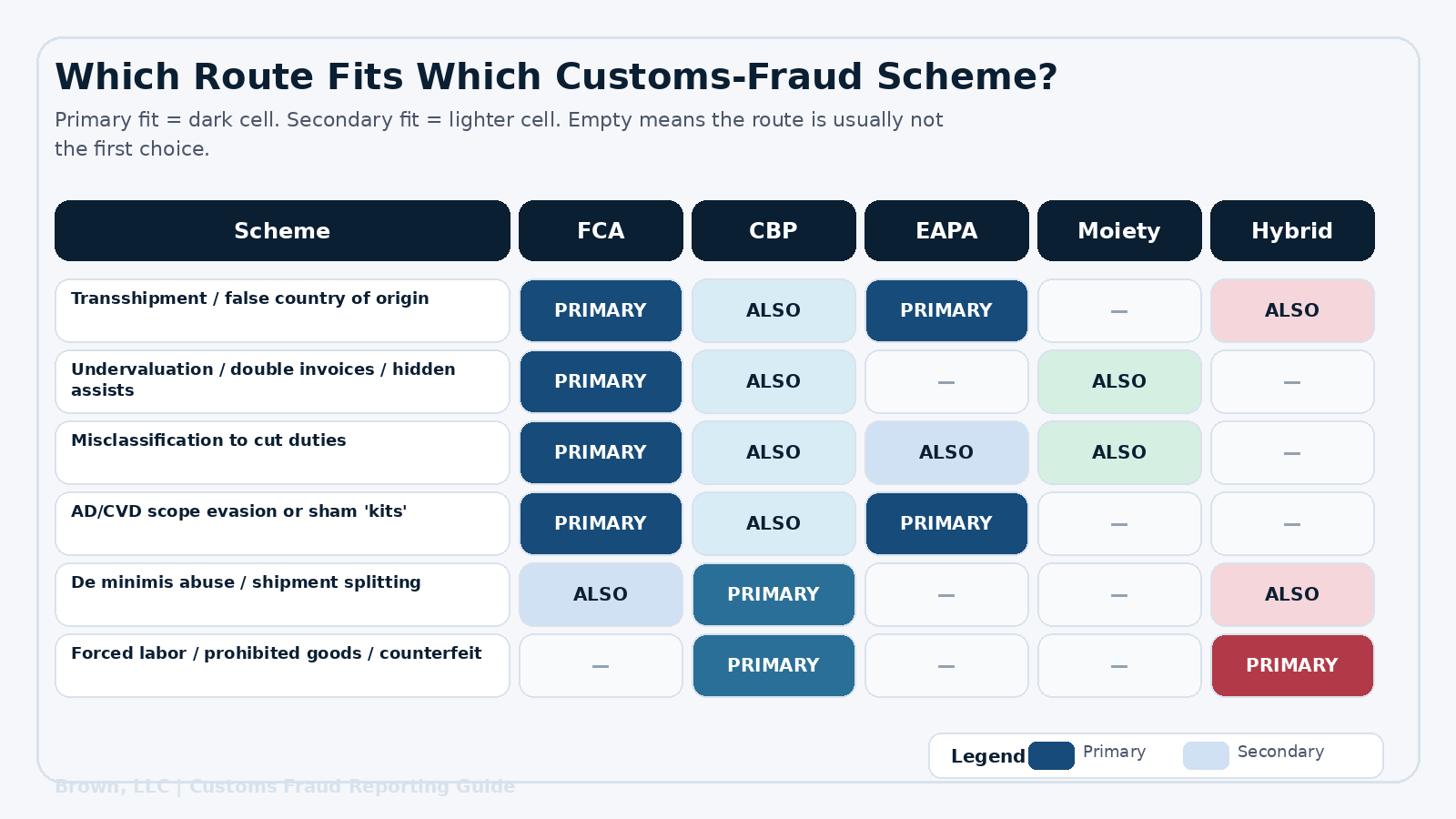

Which Customs-Fraud Scheme Fits Which Reporting Lane?

This is where many people need the clearest answer.

1. Transshipment Through a Third Country

If goods are really from China but are being repackaged, lightly processed, or rerouted through another country to dodge duties, that may support:

- FCA if the underpayment theory is strong and the damages are serious

- EAPA if the problem is AD/CVD evasion and the reporter qualifies as an interested party

- CBP e‑Allegations if the reporter needs a quick agency report or does not fit the FCA/EAPA posture yet

2. Undervaluation or Double-Invoicing

If the importer is underreporting value, hiding assists, or using alternate invoices to reduce duties, the strongest path is often:

- FCA for a serious reverse-false-claims presentation

- CBP e‑Allegations if the facts are strong enough for a trade tip but not yet packaged as a qui tam matter

3. Misclassification to Reduce Duties

If the importer is using false tariff classifications or manipulating product descriptions, the likely routes are:

- FCA when the knowing avoidance of duties is material and large

- EAPA when the misclassification relates to AD/CVD-covered merchandise

- CBP e‑Allegations for direct trade reporting

4. False Scope Claims or Sham Kits

Recent DOJ cases show that “creative” product descriptions and sham packaging strategies can create liability. These cases often belong in:

- FCA, especially if the company knowingly used false customs forms or failed to correct prior false declarations

- EAPA, when the conduct concerns covered merchandise and AD/CVD obligations

5. De Minimis Abuse or Shipment-Splitting

This is one of the more contemporary trade-enforcement issues. If importers are splitting shipments, manipulating declared values, or abusing de minimis pathways, the likely first lane is often:

- CBP e‑Allegations for a fast trade-enforcement report

- potentially FCA if the scheme is large enough and tied to deliberate avoidance of duties owed to the government

6. Forced Labor, Prohibited Goods, or Counterfeit Issues

These cases often call for CBP and potentially criminal or hybrid reporting, not just an FCA analysis. Some may have customs-duty components. Some may not. The wrong move is assuming every border-fraud problem is best framed only as an FCA damages case.

What Evidence Matters Most in a Customs-Fraud Case?

The strongest customs cases usually turn on documents that show knowledge, not just errors. That can include:

- entry summaries and customs declarations

- invoices and alternate invoices

- packing lists and bills of lading

- country-of-origin certificates and supplier communications

- broker instructions

- internal emails about classification, valuation, scope, or origin

- compliance memos

- AD/CVD analyses or scope discussions

- corrections that were discussed but never made

- data showing repeated entries using the same false pattern

In a customs case, the government often wants to understand three things:

- What duty or obligation was really owed?

- What statement or omission caused CBP to assess less?

- Who knew the truth inside the company or the supply chain?

That is why internal communications can matter so much.

What Not to Do Before You Report Customs Fraud

Do Not Assume Every Customs Problem Belongs in an FCA Case

Some do. Some do not. AD/CVD evasion may call for EAPA. Counterfeit or forced-labor issues may call for direct CBP attention. Smaller cases may not justify a heavy qui tam build.

Do Not Assume a CBP Portal Report Secures an FCA Reward Path

It does not. A CBP tip and a sealed FCA filing are different things.

Do Not Over-Collect Documents

The strongest whistleblower is not always the person with the biggest file dump. It is the person whose evidence is targeted, relevant, and lawfully handled.

Do Not Use Company Systems to Plan Your Reporting Strategy

That includes company email, company chat, shared drives, and monitored devices.

Do Not Alert the Wrong People Too Early

If the scheme is deliberate, tipping off management, brokers, or supply-chain participants too early can change the evidence picture quickly.

Do Not Wait While the Company Self-Discloses

Recent DOJ customs resolutions show that voluntary self-disclosure, cooperation, and remediation can affect company treatment. That is one more reason insiders and competitors need to think about timing.

How Do I Report Customs Fraud to CBP?

The most direct CBP route is usually the agency’s Trade Violation Reporting / e‑Allegations system. DOJ has also publicly said that tips and complaints from all sources about potential customs fraud can be reported to CBP.

Is a CBP E‑Allegation the Same as a False Claims Act Case?

No. A CBP portal report is a trade-enforcement tip. A False Claims Act case is a sealed federal court filing with its own reward structure and procedural rules.

What Is EAPA?

EAPA is the Enforce and Protect Act framework for investigating AD/CVD evasion. It is not a general customs-fraud process. It is available to qualifying interested parties and focuses on covered merchandise subject to antidumping or countervailing duty orders.

What Is a Moiety Claim in Customs Fraud?

It is a customs informant compensation route under 19 U.S.C. § 1619. The award can be up to 25% of the net recovery, but it is capped at $250,000 per case.

Can I File a Customs-Fraud FCA Case Without a Lawyer?

A relator can file an FCA complaint, but a qui tam case is not something a person can litigate pro se on behalf of the United States. In practice, serious FCA customs cases require counsel.

Can a Former Employee Report Customs Fraud?

Yes. Former employees, competitors, brokers, vendors, and other knowledgeable sources can all be relevant sources of information. The right reporting lane depends on the facts, the size of the case, and the route that best fits the conduct.

What Is Usually the Best Route if the Case Is Large?

If the case involves major underpaid duties and strong nonpublic evidence of knowing misconduct, the False Claims Act often deserves first analysis because it can offer seal, DOJ involvement, and a reward path that is materially different from CBP-only routes.

The most contemporary and under-owned customs-fraud question is not just whether customs fraud violates the False Claims Act. It is how to report customs fraud intelligently in a world where DOJ, CBP, HSI, and administrative trade processes are all active at the same time. That is why the best first move in a serious customs matter is often not a portal submission, not a hotline, and not guesswork.

It is counsel first. A quality customs-fraud whistleblower lawyer can decide whether the case belongs in a sealed FCA filing, a CBP e‑Allegation, an EAPA allegation, a moiety claim, a criminal referral strategy, or some combination of them. That choice can affect the recovery, the leverage, the confidentiality, and the outcome.