Skip to main content

Skip to main content

How to Put Together a Successful IRS Whistleblower Case: Form 211, Evidence, Awards, and Lawyer Strategy

Table of Contents

IRS whistleblower cases are different from most whistleblower cases and the program has traps and zaps and could take almost a decade if not more for a successful outcome. You do not file a lawsuit like a False Claims Act case. You do not simply submit a short tip and hope the government figures it out. And you should not assume that a suspicion of tax fraud is enough. You have one bit at the apple and if you don’t silver platter it perfectly, your golden apple will become a rotten apple real quick.

A serious IRS whistleblower case is built. It is organized. It is supported by evidence. It identifies the taxpayer, the tax years, the tax theory, the likely underpayment, the documents that prove it, and why the IRS should care. For each step that you miss or come up short, the IRS will assume you don’t have the goods and most likely move on, that’s why you need to show them that you have concrete information that’s likely to result in a big enforcement and that you have the firepower to answer all their factual and legal questions – thus hiring one of the best IRS whistleblower law firms is critical.

Speak with the Lawyers at Brown, LLC Today!

Over 100 million in judgments and settlements trials in state and federal courts. We fight for maximum damage and results.

The IRS itself says a whistleblower claim should include specific and credible allegations, supporting documents, and an explanation of how and when the whistleblower learned about the violation. The IRS also states that awards are generally 15% to 30% of the amount collected because of the whistleblower’s information.

That sounds simple. It is not. The IRS whistleblower program can produce significant awards, but it is not designed for guesses, workplace grievances, or weak suspicions. The strongest cases usually involve major tax underpayments, lawful access to strong evidence, and a realistic path for the IRS to collect.

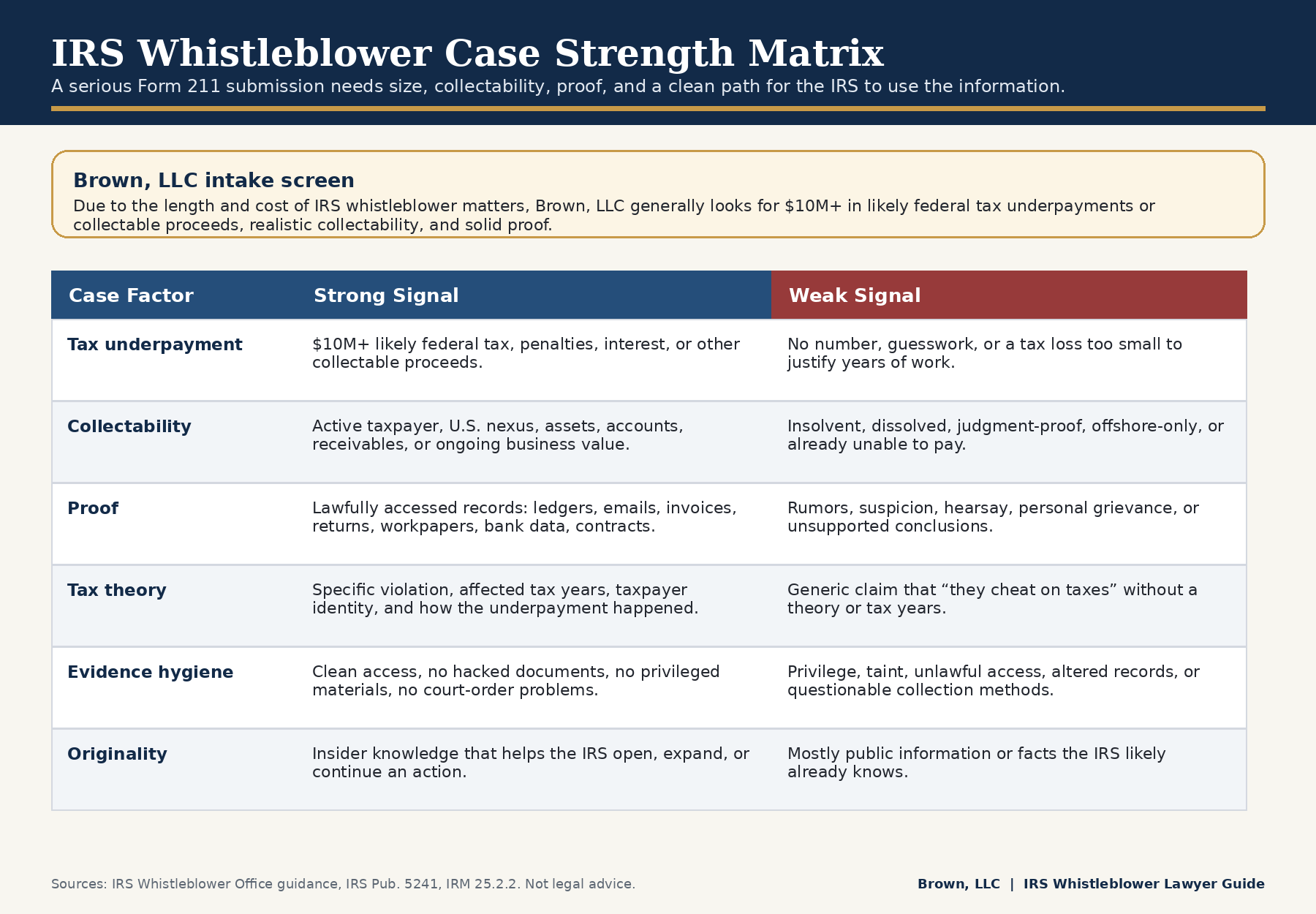

Important Brown, LLC Tax Fraud Intake Note: IRS Cases Must Be Large, Collectable, and Well-Proven

Because IRS whistleblower cases can take years and require substantial attorney time, financial analysis, tax review, document organization, and government-facing advocacy, Brown, LLC generally evaluates IRS whistleblower cases only when all three conditions are present:

- At least $10 million in likely federal tax underpayments, penalties, interest, or other collectable proceeds;

- Realistic collectability, meaning the taxpayer likely has assets, income, accounts, operating business value, insurance, U.S. nexus, or other reachable sources of payment;

- Solid proof, not speculation — such as internal accounting records, emails, ledgers, tax schedules, offshore account information, false deductions, transfer-pricing materials, invoices, contracts, or other lawfully obtained evidence.

This is not the IRS’s legal threshold. The IRS mandatory award track under IRC § 7623(b) generally requires proceeds in dispute exceeding $2 million and, for individual taxpayers, gross income exceeding $200,000 for at least one relevant tax year.

Brown, LLC’s threshold is higher because the practical reality is harsher. IRS cases are long. Awards cannot generally be paid until the taxpayer’s appeal rights and refund-claim rights are exhausted, which means award payments may not happen for several years after filing.

That is why serious screening matters. And screening on top of screening. A smaller case may still be reportable. It may even fit another legal path. But for a firm like Brown, LLC that is in high demand to invest in an IRS whistleblower matter, the case usually needs to be large enough, collectable enough, and provable enough to justify the fight.

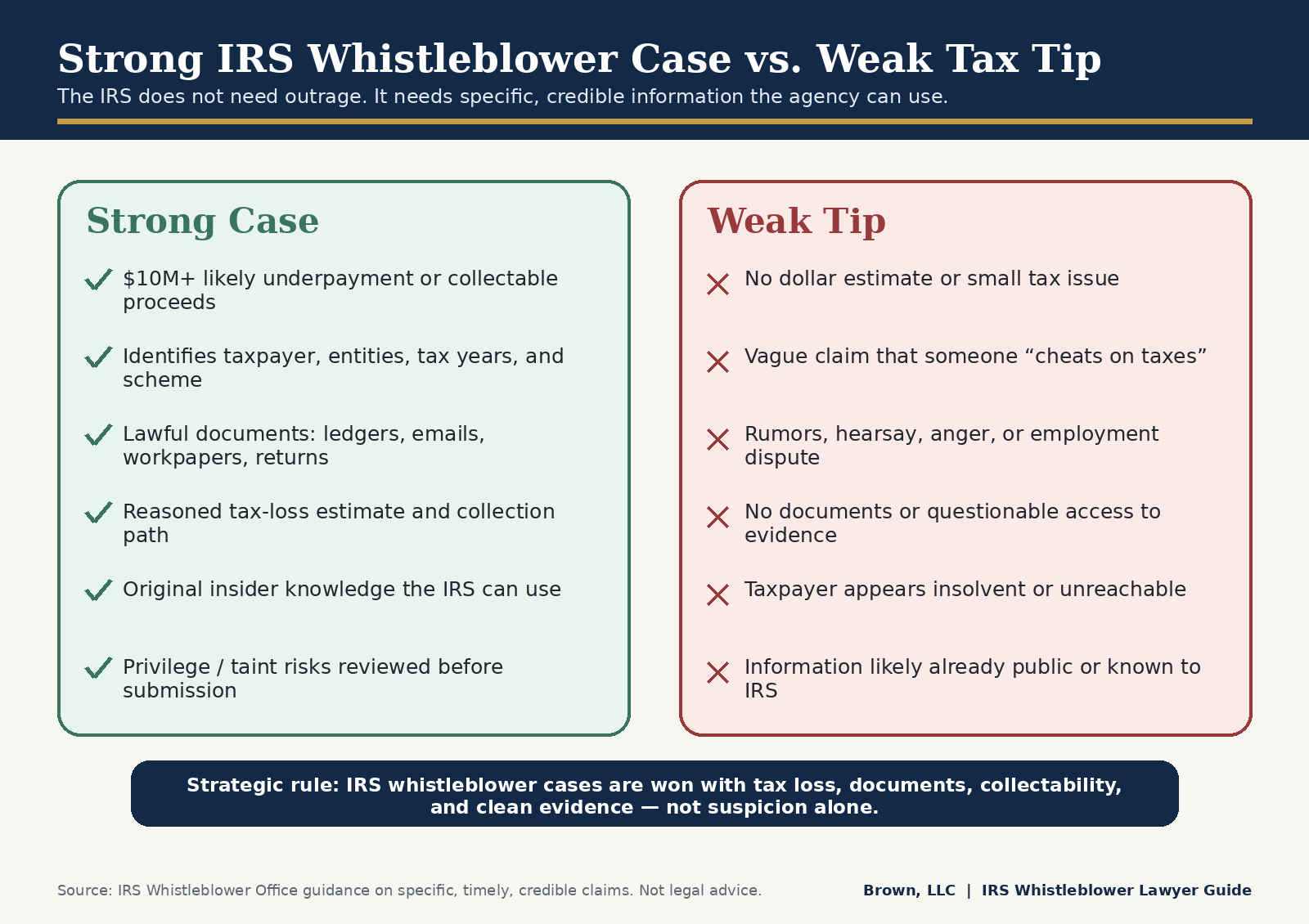

The Single Biggest Mistake IRS Whistleblowers Make – “I Think”

The biggest mistake is submitting a suspicion instead of a case. A suspicion sounds like this: “I think the company is hiding income.” Or “Upon information and belief.”

A case sounds like this: “For tax years 2021 through 2024, Company X booked revenue through Entity Y, which was controlled by the same owners, but omitted that income from its U.S. federal returns. The internal ledgers, bank records, emails, and tax schedules show approximately $18 million in unreported taxable income and here is the year by year deficiency itemization, the violation of the tax code, and comparable enforcement actions.”

That is the difference. IRS whistleblower cases are not won by dirty laundry with speculation. They are won by tax loss, documents, credibility, factual and legal presentation and collection potential.

What the IRS Needs to See for a Successful IRS Whistleblower Award

A strong IRS whistleblower submission should answer these questions clearly:

-

Who is the taxpayer?

Identify the person, company, partnership, trust, estate, nonprofit, promoter, or related entity involved. Include known names, addresses, EINs, SSNs if lawfully known, affiliated entities, owners, officers, and responsible professionals.

-

What tax law was violated?

Do not just say “tax fraud.” Identify the conduct. Cite to the statutes and regulations and point to successful previous enforcement actions. Examples of underlying conduct include:

- underreported income

- false deductions

- sham entities

- inflated basis

- improper transfer pricing

- abusive conservation easements

- offshore accounts

- payroll tax evasion

- employment tax fraud

- false charitable deductions

- nominee ownership

- cryptocurrency concealment

- unpaid excise taxes

- fraudulent refund claims

- false Forms 1099, W-2, K-1, or partnership reporting

-

What tax years are involved?

The submission should identify the relevant tax years and explain whether the conduct is ongoing.

-

How much is likely owed?

This is critical. The best IRS whistleblower submissions do not merely describe misconduct. They estimate the underpayment. The estimate does not need to be perfect, but it should be reasoned. A serious submission should explain:

- omitted income

- improper deductions

- unpaid tax

- penalties

- interest

- related-party flows

- affected entities

- collectable proceeds

-

What proof supports it?

The IRS asks for documents that support the allegation. Good proof may include:

- internal accounting records

- bank records

- invoices

- contracts

- board presentations

- tax workpapers

- audit memos

- emails

- spreadsheets

- general ledgers

- entity charts

- foreign account information

- payroll records

- K-1s

- W-2s

- Forms 1099

- tax return excerpts

- communications with accountants

- documents showing ownership or control

-

How did you learn the information?

Form 211 requires the whistleblower to explain how and when they learned about the alleged violation. Original, inside information is usually stronger than public information.

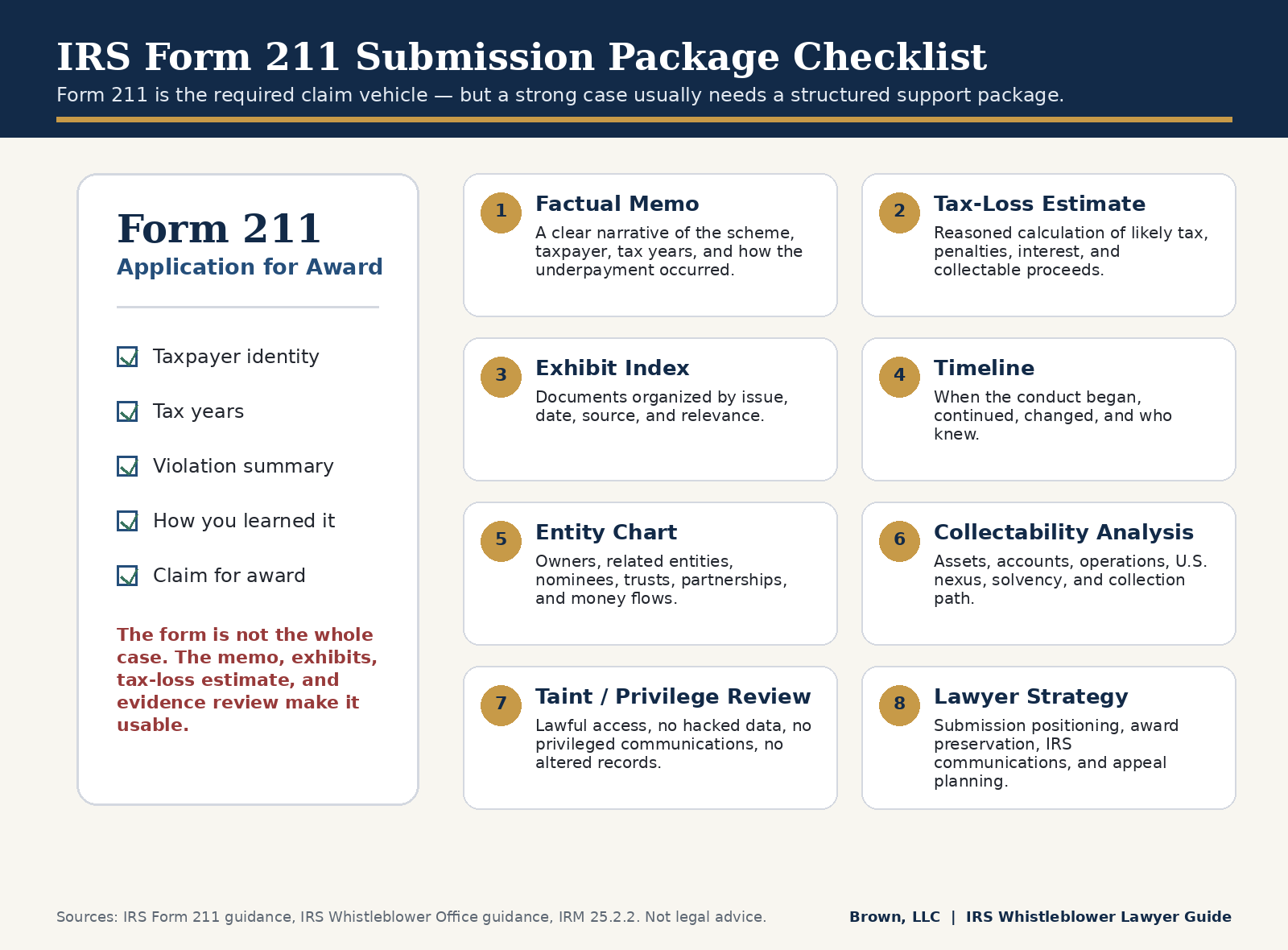

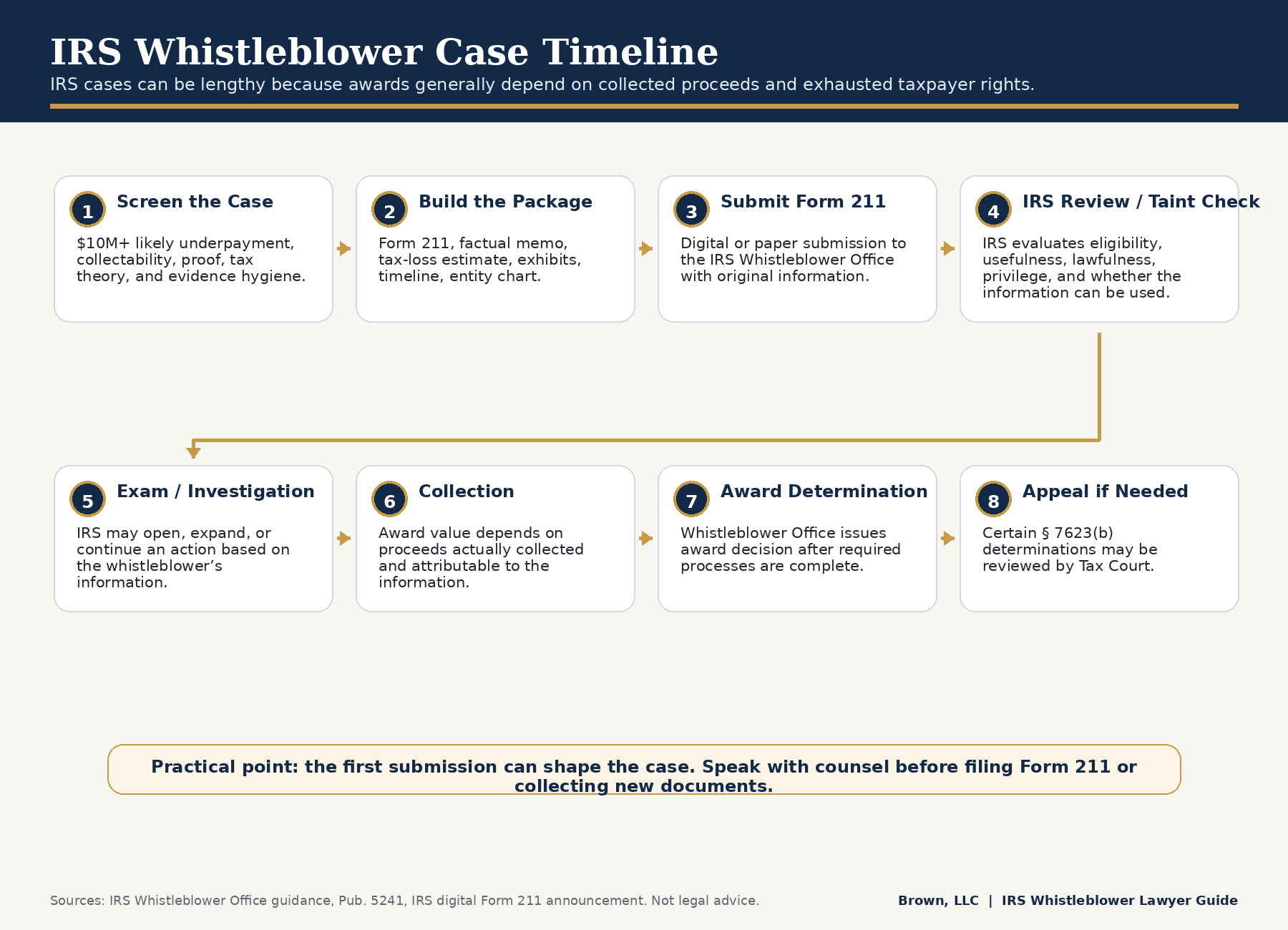

Why Form 211 Is Not Enough by Itself

Form 211 is the required IRS whistleblower form. But the form itself is not the case.

A strong submission usually includes:

- completed Form 211

- legal and factual memorandum

- exhibit list

- timeline

- damages or tax-loss estimate

- witness list

- entity chart

- document index

- explanation of collection potential

- privilege and taint analysis if needed

The IRS Internal Revenue Manual states that a whistleblower must submit Form 211 claiming an award before the IRS proceeds with an action based on the whistleblower’s information. That timing point is important. A whistleblower should not casually send information in the wrong format and assume award rights are protected. The IRS now permits secure digital Form 211 submissions, which is a major update from older guidance that discussed only paper submission. But the strategic point remains the same: the form should be supported by a serious submission package.

The Evidence Matrix: What Makes an IRS Case Strong

A successful IRS whistleblower case usually has evidence in several categories.

| Evidence Category | Strong Example | Weak Example |

| Taxpayer identity | EIN, entity chart, owners, related companies | “I think they use shell companies” |

| Tax years | 2021–2024 returns and internal ledgers | “This has been going on for years” |

| Tax violation | False deductions, omitted income, offshore concealment | “They cheat on taxes” |

| Dollar estimate | $10M+ tax underpayment with supporting calculation | No dollar estimate |

| Documents | Emails, ledgers, bank records, tax schedules | Rumors or verbal statements only |

| Knowledge | Emails showing executives/accountants knew | “Everyone knew” |

| Collectability | Active company, assets, accounts, U.S. operations | Dissolved entity with no assets |

| Originality | Insider documents and firsthand knowledge | Public news article only |

This is the kind of practical detail most competing articles do not provide.

Why Collectability Matters

A case can be legally strong but economically weak. IRS awards are based on collected proceeds. The IRS’s FY 2024 Annual Report states that awards are paid from proceeds collected, and payment generally cannot occur until the taxpayer has exhausted appeal rights and can no longer seek return of the proceeds.

So the question is not only:

“Did the taxpayer cheat?”

The question is also:

“Can the IRS collect?”

A strong case should consider:

- Does the taxpayer still exist?

- Does the taxpayer have assets?

- Is the taxpayer in the United States?

- Are there bank accounts, real estate, receivables, or business operations?

- Is the taxpayer solvent?

- Are there responsible persons or related entities?

- Are there alter ego, nominee, transferee, or offshore collection issues?

- Are the relevant years still actionable?

Brown, LLC’s $10 million threshold is tied to this reality. A large nominal underpayment does not help much if the taxpayer is judgment-proof, bankrupt, dissolved, offshore beyond reach, or already under collection pressure with no assets.

Do Not Create a Taint Problem

This is where many whistleblowers can hurt their own case. The IRS generally performs a taint review of information submitted with Form 211 to identify evidentiary, ethical, legal, or privilege concerns. The IRS states that taint review is used to insulate investigation functions from information that could jeopardize adjustments and collection activity, and information not used because of taint concerns will not result in proceeds for an award. That means a whistleblower should not:

- hack systems

- steal privileged communications

- take documents outside lawful access

- violate court orders

- copy personal tax records without legal guidance

- take attorney-client communications

- access files they are not permitted to access

- destroy, alter, or conceal evidence

A lawyer can help separate useful evidence from dangerous evidence. That is not a technicality. It can decide whether the IRS can use the information.

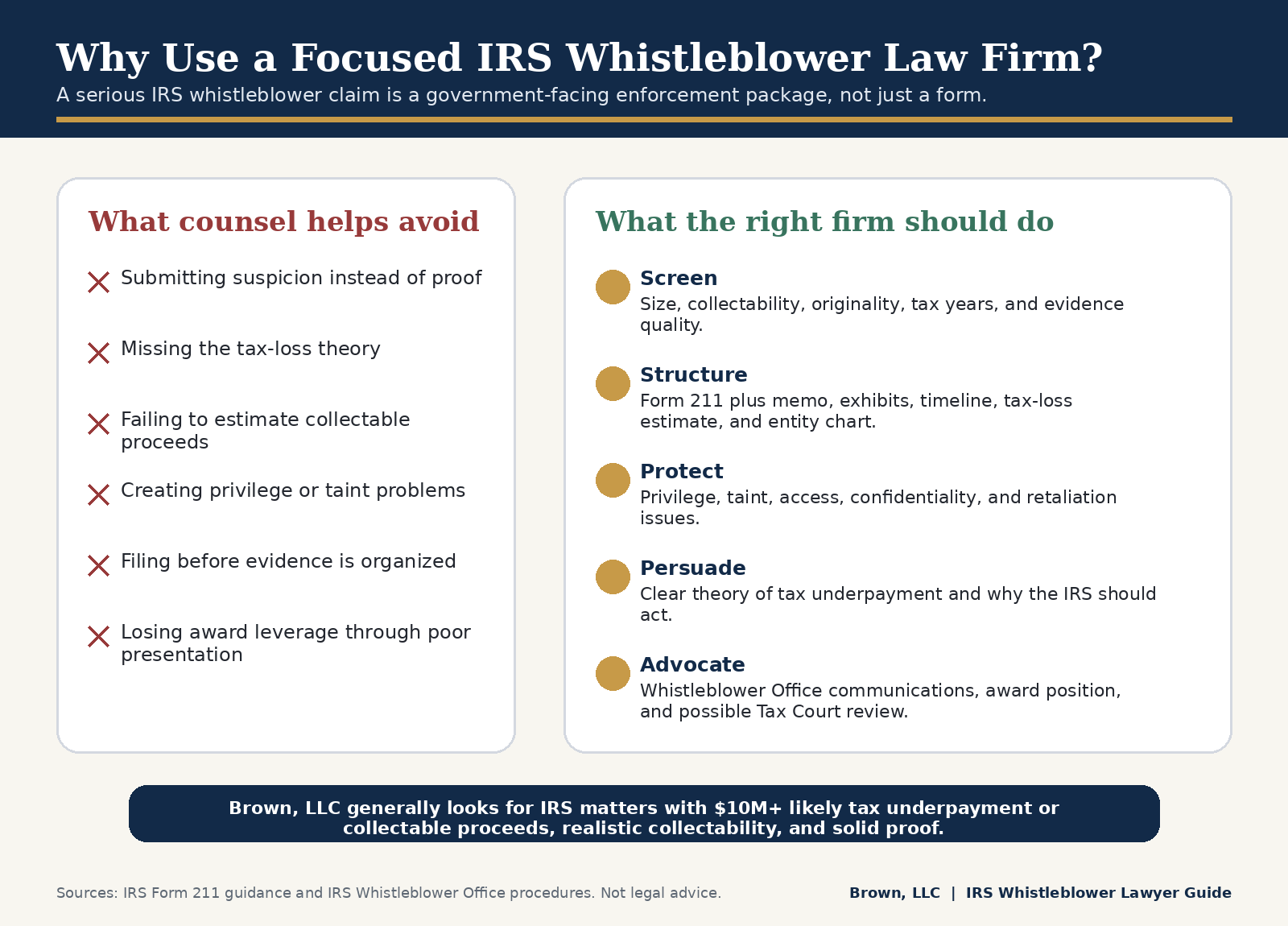

Why You Should Use an IRS Whistleblower Lawyer

There are tax tips, and then there are IRS whistleblower cases. A meaningful IRS whistleblower case should be treated like a government enforcement submission. That means the lawyer’s role is not just to “fill out Form 211.” The lawyer’s role is to help build a credible, organized, lawful, persuasive case. A focused IRS whistleblower law firm can help with:

- screening whether the case is large enough

- evaluating collectability

- estimating tax underpayment

- identifying the correct tax theory

- organizing evidence

- protecting privilege and avoiding taint

- preparing the Form 211 narrative

- drafting a legal and factual memorandum

- determining whether related programs may apply

- preserving award rights

- communicating with the Whistleblower Office

- addressing retaliation risk

- responding to award recommendations

- pursuing Tax Court review if appropriate

The IRS Internal Revenue Manual says award reports may consider how the whistleblower’s information affected the opening, expansion, or continuation of an audit, as well as the quality of the organization of the information and the quality of factual or legal analysis provided. That is the argument for counsel in one sentence. The quality of the submission matters.

Why Use a Firm Like Brown, LLC?

The best IRS whistleblower law firm is not always the one that says “yes” fastest. The best firm is often the one that pressure-tests the case before filing. IRS whistleblower cases can take years. They require patience, proof, tax analysis, and judgment. A law firm handling these cases should be willing to tell a potential client when the case is too small, too speculative, too hard to collect, or too risky to submit as framed.

Brown, LLC is a national whistleblower practice led by a former FBI Special Agent and Legal Advisor, with experience handling whistleblower claims and major fraud matters, surrounded by other former DOJ attorneys. That investigative background matters in IRS whistleblower cases because the submission must be more than a complaint. It must be a coherent enforcement package.

For the right case, Brown, LLC looks for:

- major tax underpayment

- credible insider knowledge

- lawful documents

- a clear tax theory

- a realistic collection path

- a whistleblower who can explain how they know what they know

- facts strong enough to justify years of work

That is why Brown, LLC generally requires at least $10 million in likely tax underpayments or collectable proceeds, along with solid evidence and collectability. This standard is not meant to discourage serious whistleblowers. It is meant to avoid wasting the whistleblower’s time, the IRS’s time, and the client’s emotional energy on a case that is unlikely to generate a meaningful result.

What Types of IRS Whistleblower Cases Are Usually Strongest?

The strongest IRS cases often involve sophisticated tax noncompliance, not simple mistakes. Examples include:

Offshore tax evasion

Undisclosed foreign accounts, nominee entities, offshore trusts, shell companies, or foreign income that was not reported.

Corporate income shifting

Related-party transactions used to move income away from the proper taxpayer or jurisdiction.

False deductions

Inflated expenses, fake vendors, sham consulting fees, false charitable contributions, or deductions lacking economic substance.

Payroll and employment tax fraud

Workers intentionally misclassified, payroll taxes withheld but not paid, cash payroll systems, or false employment reporting.

Partnership and pass-through abuse

Improper allocations, inflated basis, hidden distributions, false K-1 reporting, or disguised sales.

Promoter-driven schemes

Tax shelters, abusive conservation easements, syndicated deductions, or mass-marketed structures sold to taxpayers.

Crypto and digital asset concealment

Unreported gains, offshore exchanges, false basis reporting, nominee wallets, or hidden digital asset income.

High-net-worth individual evasion

Concealed income, nominee ownership, sham loans, false residency claims, or failure to report foreign assets.

What Makes a Weak IRS Whistleblower Case?

A weak case usually has one or more of these problems:

- no documents

- no tax-loss estimate

- no clear taxpayer identity

- no tax years

- no original information

- no IRS whistleblower lawyer

- no organization in terms of presentation

- purely public information

- personal vendetta

- employment dispute disguised as tax fraud

- taxpayer lacks assets

- information may be privileged or improperly obtained

- alleged tax loss is too small

- the IRS already knows the information

- statute of limitations problems

- vague claims like “they are cheating”

A lawyer can sometimes fix a weak presentation. A lawyer cannot create facts that do not exist.

How to Prepare Before Calling an IRS Whistleblower Lawyer

Before contacting counsel, prepare a clean, factual summary. Do not send privileged documents or take new documents without legal advice. But do organize what you already lawfully have. Useful preparation includes:

-

Name the taxpayer.

Identify the company, individual, trust, partnership, or related entities.

-

Identify the tax years.

State when the conduct happened and whether it is ongoing.

-

Describe the scheme.

Use plain English. Explain how the underpayment happened.

-

Estimate the tax loss.

Even a rough calculation is better than none.

-

List the proof.

Identify documents, witnesses, emails, records, ledgers, accounts, or returns.

-

Explain your role & Put any taint issues front and center.

State how you learned the information. Potentially request a taint team – that means if you lawfully obtained the information but there may be issues of accounting or legal privilege let the IRS whistleblower law firm know first!

-

Assess collectability.

Explain whether the taxpayer has assets or ongoing business operations.

-

Flag risk issues.

Identify privilege, confidentiality, employment, or document-access concerns.

That information allows a serious IRS law firm to evaluate the case quickly.

FAQ

What is IRS Form 211?

Form 211 is the IRS form used to submit a whistleblower claim for an award. The IRS states that a whistleblower claim should include specific and credible allegations, supporting documents, and an explanation of how and when the whistleblower learned about the violation.

What is the IRS whistleblower reward?

The IRS states that a whistleblower award is generally 15% to 30% of the amount collected because of the whistleblower’s information.

What is the IRS mandatory award threshold?

For IRC § 7623(b), the IRS annual report explains that the claim generally must involve proceeds in dispute exceeding $2 million, and if the taxpayer is an individual, that person’s gross income must exceed $200,000 for at least one relevant tax year.

Does Brown, LLC take every IRS whistleblower case?

No. Brown, LLC generally evaluates IRS whistleblower cases only when there is at least $10 million in likely tax underpayment or collectable proceeds, realistic collectability, and solid proof and even with that criteria is highly selective.

How long do IRS whistleblower cases take?

IRS cases can take years. The IRS explains that awards generally cannot be paid until taxpayer appeal rights and refund-claim rights are exhausted. Right now, the wait time for a successful enforcement action could be as long as a decade, but there is legislation moving through Congress to reform the process and the timetable.

Can I submit Form 211 online?

Yes. The IRS announced the launch of a digital Form 211 in December 2025, allowing whistleblowers to submit information electronically to the Whistleblower Office.

Do I need a lawyer for an IRS whistleblower case?

You are not required to use a lawyer, but serious IRS whistleblower cases usually benefit from counsel. A lawyer can help organize the evidence, avoid taint or privilege problems, estimate tax loss, preserve award rights, and present the case in a way the IRS can actually use. It’s a tough program with big bucks at stake, so you need someone to both protect you and advance your case. Presenting the case in the best light the first time around is critical since you may only have one shot at it.

Bottom Line

A successful IRS whistleblower case is not just a tip. It is a structured enforcement submission. It should identify the taxpayer, the tax years, the tax violation, the evidence, the underpayment, the collection path, and why the IRS should act. For Brown, LLC to take an IRS whistleblower case, the matter generally must involve at least $10 million in likely tax underpayments or collectable proceeds, realistic collectability, and solid proof.

If you have credible, documented information about significant tax fraud, speak with an IRS whistleblower lawyer before filing Form 211. The first submission may shape everything that follows and determine whether your case survives the long haul and results in one of the successful IRS whistleblower awards versus goes down directly into the digital circular basket and is never seen or heard from again. Don’t turn a win into a loss, and never skimp on great attorneys or accountants, a healthy percentage of an IRS whistleblower awards is much better than 100% of zero – if you have information about large scale tax cheats speak with one of the best IRS whistleblower law firms and learn your rights.